Transit Asset Management: Archived Questions and Answers

The questions included on this page address the requirements for complying with the Transit Asset Management (TAM) rule are set forth in 49 CFR part 625. These FAQs are not a substitute for reviewing the TAM rule. The questions are grouped together by topic area to help you find what you are looking for.

- What is transit asset management?

- What is the TAM rule?

- How is the TAM plan linked to Public Transportation Agency Safety Plan (PTASP)?

- Who must comply with the TAM rule?

- How do transit providers comply with the TAM rule?

- Am I a tier I or tier II agency?

- My agency is the public transportation provider for a tribal government. What are we responsible for under the TAM rule?

- How will FTA ensure compliance with the TAM rule?

- Which 5310 grantees are exempt from the TAM rule?

- What deadlines must I comply with under the TAM rule?

- How does TAM rule compliance impact the allocation of federal funds?

- What is a transit asset management plan (TAM plan)?

- What process must I follow to develop a TAM plan?

- Does FTA require TAM plans to be submitted by October 1, 2018?

- What is the requirement for Board action for TAM plans? Do they need to pass a resolution or vote in the minutes or some other acknowledgement?

- What level of change requires a complete TAM plan update?

- Does FTA require that TAM plans be signed by agency leadership?

- Who must be the sponsor of a group TAM plan?

- Who is allowed to participate in a group TAM plan?

- Where can I find more information about MPO Coordination and Statewide TAM Targets?

- What does “annual condition assessment report” in rule section 625.53(b) mean?

- Which facilities require a condition assessment?

- What method must I use for conducting condition assessments of assets?

- How do I know if I have direct capital responsibility for an asset?

- Do I have capital responsibility for a shared use facility?

- What must be reported when a facility is shared?

- What is a useful life benchmark?

- What is the difference between the TAM ULBs and the useful lifedefinition used in FTA's grant programs?

- The Default ULB Cheat Sheet states that transit agencies can adjust their ULB with approval from FTA. Can FTA provide guidance on the process?

- What does a high or low performance target value mean?

- Who needs to approve the TAM Performance Measure targets before we submit them to the MPO?

- Do MPOs have to update their TAM targets annually? Even if they update their TIP or MTP more frequently than Planning regulations require?

- What is the difference between assets in my TAM plan and NTD inventory and targets?

- We have fixed guideway assets, but we don’t operate rail fixed guideway. Am I Tier I or Tier II? Do I need to set Infrastructure category targets?

- What does the $50,000 threshold refer to?

- Does the $50,000 threshold mean $50,000 in total equipment value, or $50,000 per unit of equipment?

- What about equipment in a facility?

- Do IT systems hardware and software systems need to be included in equipment category?

General

What is transit asset management?

Transit asset management (TAM) is the strategic and systematic practice of procuring, operating, inspecting, maintaining, rehabilitating, and replacing transit capital assets to manage their performance, risks, and costs over their life cycles to provide safe, cost-effective, and reliable public transportation. TAM uses transit asset condition to guide how to manage capital assets and prioritize funding to improve or maintain a state of good repair.

What is the TAM rule?

The TAM rule (49 CFR part 625) is a set of federal regulations that sets out minimum asset management practices for transit providers. The current estimated cost to bring all of the nation’s transit assets into a state of good repair is $89.8 billion. FTA estimates that annually $17.0 billion of capital investment would be needed get the nation’s transit systems to a state of good repair. This is 8.6 percent higher than is currently spent on asset preservation and expansion combined. The TAM rule aims to address the backlog by requiring transit providers to create TAM plans that will help them systematically address their maintenance needs which will, in turn, improve service. Well-developed asset management systems have been shown to lower long-term maintenance costs. Additionally, TAM will have important non-quantifiable benefits, such as improved transparency and accountability. Implementing a TAM system will require transit providers to collect and use asset condition data, set targets, and develop strategies to prioritize investments to meet their goals.

The purpose of the FTA rulemaking is to help achieve and maintain a state of good repair (SGR) for the nation’s public transportation assets. Currently, there is an estimated $89.8 billion transit SGR backlog. The rule develops a framework for transit agencies to monitor and manage public transportation assets, improve safety, increase reliability and performance, and establish performance measures.

How is the TAM plan linked to Public Transportation Agency Safety Plan (PTASP)?

In July 2018, FTA published the Public Transportation Agency Safety Plan (PTASP) final rule (49 C.F.R. Part 673) to improve public transportation safety by guiding transit agencies to more effectively and proactively manage safety risks in their systems. It requires certain recipients and sub-recipients of FTA grants that operate public transportation to develop and implement safety plans that establish processes and procedures to support the implementation of Safety Management Systems (SMS).

Through the implementation of the Transit Asset Management (TAM) Plan, required under 49 C.F.R. Part 625, a transit agency should consider the results of its condition assessments while performing safety risk management and safety assurance activities. The results of the condition assessments, and subsequent SMS analysis could inform a transit agency’s TAM Plan elements, specifically investment priorities. The Accountable Executive has the ultimate responsibility for decision-making throughout this process and for approving both the TAM plan and the PTASP.

Please note, the PTASP final rule applies to only Section 5307 recipients and sub-recipients, and the TAM rule applies to all operators of public transit.

You can find more information on FTA’s PTASP website, including an infographic on the nexus between TAM and SMS.

Compliance

Who must comply with the TAM rule?

The TAM rule applies to all recipients of Chapter 53 funds that either own, operate, or manage capital assets used in providing public transportation services.

| The rule applies to you | The rule does NOT apply to you |

|---|---|

| If you own an FTA-funded capital asset used in providing public transportation services, then you must comply with the TAM rule, even if you do not operate or manage that asset. | If you do not receive Chapter 53 funds and you have never received Chapter 53 funds, then the TAM rule does not apply to you. |

| If you manage or operate an FTA-funded capital asset used in providing public transportation services, then you must comply with the TAM rule, regardless of who owns that asset. | If you receive FTA funds, but do not use those funds for public transportation services, then the TAM rule does not apply to you (e.g., Planning or Research grants) |

NOTE: Public Transportation is defined by law as “regular, continuing shared-ride surface transportation services that are open to the general public or open to a segment of the general public defined by age, disability, or low income.” 49 U.S.C. § 5302(14).

An example of public transportation service to a segment of the general public is service for all senior citizens or all persons with disabilities in a particular town or county. However, if you are providing a courtesy shuttle service for patrons of a specific establishment with a senior citizen clientele, then your service is not considered to be public transportation. Similarly, if you provide service that requires membership in an organization such as a church or club, then, your service is not considered to be public transportation.

In addition, commuter rail service providers operating on the Northeast Corridor (NEC) should also reference 49 USC §24904(c) for additional asset management regulations.

How do transit providers comply with the TAM rule?

Transit providers must complete several key actions to comply with the TAM rule, including developing a TAM plan and submitting two reports to the NTD annually: a data report and a narrative report. More detailed descriptions of each requirement will follow in the FAQ.

Develop TAM plan. All transit agencies that own, operate, or manage capital assets used in the provision of public transportation and receive federal financial assistance under 49 U.S.C. Chapter 53 either as recipients or subrecipients must develop a TAM plan. A TAM plan is a tool that will aid transit providers in:

- Assessing the current condition of its capital assets

- Determining what the condition and performance of its assets should be (if they are not already in a state of good repair)

- Identifying the unacceptable risks, including safety risks, in continuing to use an asset that is not in a state of good repair

- Deciding how to best balance and prioritize reasonably anticipated funds (revenues from all sources) towards improving asset condition and achieving a sufficient level of performance within those means

TAM plans must include at a minimum an asset inventory, condition assessments of inventoried assets, and a prioritized list of investments to improve the state of good repair of their capital assets.

Complete NTD asset inventory module (AIM) report. You must develop an inventory of your assets, and you must report the data and other information required to the NTD asset inventory module report annually. Additional data required by NTD includes information used to calculate the TAM metrics.

Conduct and report facility condition assessments. You must assess the condition of all the capital assets in your TAM plan, and you must report the condition assessments for facility category assets to the NTD for a portion of your agency’s facility capital assets. Every year thereafter, you must report the condition assessments for another proportion of your agency’s facility capital assets, until all of the condition assessments for all facility capital assets have been reported to the NTD. You must then renew the process of conducting condition assessments.

Set Performance Targets. You must set targets annually for the performance of your assets and submit those targets to the NTD as part of your annual data submission. Each asset category has its own performance measure by which to set targets:

- Rolling stock: % of revenue vehicles exceeding ULB

- Equipment: % of nonrevenue service vehicles exceeding ULB

- Facilities: % of facilities rated under 3.0 on the TERM scale

- Infrastructure: % of track segments under performance restriction

Submit narrative report to the NTD. You must submit an annual narrative report to the National Transit Database that provides a description of any change in the condition of the provider’s transit system from the previous year and describes the progress made during the year to meet the performance targets set in the previous reporting year.

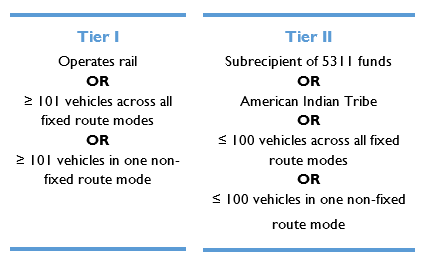

Am I a tier I or tier II agency?

The TAM final rule divides providers into two size categories: tier I and tier II. The FTA has developed a checklist to help you determine which tier applies to you.

You are a tier I agency if you:

- Operate rail

- Own, operate, or manage 101 or more vehicles in revenue service during peak regular service across all fixed route mode of transportation

- Own, operate, or manage 101 or more vehicles in revenue service during peak regular service in one non-fixed route mode of transportation

You are a tier II agency if you:

- Own, operate, or manage 100 or less vehicles in revenue service during peak regular service across all non-rail fixed route modes

- Own, operate, or manage 100 or less vehicles in revenue service during peak regular service in any one non-fixed route mode

- Are a subrecipient under the 5311 Rural Area Formula Program

- Are an American Indian tribe

My agency is the public transportation provider for a tribal government. What are we responsible for under the TAM rule?

The TAM Rule characterizes all tribal transportation providers as Tier II providers, regardless of size. This means you have the option to either develop your own TAM plan or join your State DOT’s group TAM plan, if the tribe receives funds through the State DOT. If the tribe only receives 5311(c) funds directly through FTA, then it can participate in the State group plan by mutual consent between the State and the tribe’s accountable executive, which can be the Tribal Chairman or CEO equivalent. In addition, the 5311(c) only tribe could choose to develop its own plan, or serve as the Sponsor of a tribal group plan.

How will FTA ensure compliance with the TAM rule?

Starting in FY 2019, Triennial Reviews and State Management Reviews will include TAM as a part of the FTA’s oversight review program. FTA is in the process of developing oversight standards for TAM activities and will make guidance available when it is complete. Oversight reviews will reflect objective compliance with the TAM rule. Other oversight tools such as Enhanced Review Modules and Technical Assistance are also being developed to provide more specified TAM oversight.

Adhering to the TAM requirements is also incorporated into the master agreement for direct recipient of FTA grants and in the Certifications and Assurances process. The oversight process verifies the information each recipient certified.

Which 5310 grantees are exempt from the TAM rule?

The TAM rule applies to chapter 53 recipients and subrecipients that own, operate, or manage capital assets used to provide public transportation. 49 C.F.R. § 625.3. The term "public transportation" is defined at 49 U.S.C. § 5302(14) and means regular, continuing shared-ride surface transportation services that are open to the general public or open to a segment of the general public defined by age, disability, or low income; and does not include:

- intercity passenger rail transportation provided by the entity described in chapter 243 (or a successor to such entity) of Title 49,

- intercity bus service,

- charter bus service,

- school bus service,

- sightseeing service,

- courtesy shuttle service for patrons of one or more specific establishments, or

- intra-terminal or intra-facility shuttle services.

Recipients and subrecipients of funds under 49 U.S.C. 5310(b)(1)(D) for alternatives to public transportation that assist seniors and persons with disabilities with transportation are exempt from the requirements of the TAM rule because assets funded under the program are not used to provide “public transportation.” For example, the Arc of Prince George’s County, Maryland provides programs and support services for persons with developmental disabilities. Arc receives 5310(b)(1)(D) program funds and uses the funds to provide transportation services for its clients. Arc is exempt from the TAM rule because the 5310(b)(1)(D) funded assets are used to provide client-based transportation services, instead of public transportation.

Please note, participation in coordination of public transportation and human services transportation services will not automatically make 5310(b)(1)(D) recipients or subrecipients subject to the TAM rule. However, recipients and subrecipients of 5310(b)(1)(D) that also receive section 5307 or section 5311 funds are required to comply with the requirements of the TAM rule for their 5307 and 5311 funded public transportation services and assets.

What deadlines must I comply with under the TAM rule?

Depending on when your fiscal year runs, you have the following deadline requirements for complying with TAM Rule components:

If your fiscal year runs |

July-

|

Oct-

|

Jan-

|

|---|---|---|---|

| - Share initial targets with planning partners | July2017 | ||

| - Report FY17 asset inventory module (AIM) data to NTD - Submit targets for FY18 to NTD (optional) |

Oct 2017 |

Jan 2018 |

Apr 2018 |

| - Complete compliant TAM Plan (1st required) - Share TAM Plan with planning partners |

Oct 2018 | ||

| - Report FY18 AIM data to NTD (1st required) - Submit targets for FY19 to NTD (1st required) |

Oct 2018 |

Jan 2019 |

Apr 2019 |

| - Report FY19 AIM data to NTD - Submit targets for FY20 to NTD - Submit narrative report to NTD (1st required) |

Oct 2019 |

Jan 2020 |

Apr 2020 |

| - Report FY20 AIM data to NTD - Submit targets for FY21 to NTD - Submit narrative report to NTD |

Oct 2020 |

Jan 2021 |

Apr 2021 |

| - Complete Updated TAM Plan - Share TAM Plan with planning partners |

Oct 2022 | ||

How does TAM rule compliance impact the allocation of federal funds?

At present, neither compliance with the TAM rule nor any TAM-related materials collected by FTA impacts the allocation of any federal funds.

TAM Plans

What is a transit asset management plan (TAM plan)?

The 2012 Asset Management Guide specifies that in general, an asset management plan outlines the activities that will be implemented and resources applied to address the asset management policy and strategy. For many transit agencies, the plan will address the activities and changes to be implemented to increase the maturity of asset management practice.

Primarily, asset management plans have two major components:

- Enterprise-wide implementation actions that provide enabling support and direction for asset management across all asset classes and services.

- Direction and expectations for asset class owners and department managers regarding lifecycle management planning and processes—with a focus on the lifecycle management plans (see later in this section).

Plans should outline how people, processes, and tools come together to address the asset management policy and goals. They also provide accountability and visibility for increasing the maturity of asset management practices, and can be used to support planning and budgeting activities, communicating to internal and external stakeholders, and as an accountability mechanism.

The TAM Rule requires every transit provider that receives federal financial assistance under 49 U.S.C. Chapter 53 to develop a TAM plan or be a part of a group TAM plan prepared by sponsor. All TAM plans must contain:

- An inventory of assets

- A condition assessment of inventoried assets

- Documentation of the use of a decision support tool

- A prioritization of investments

Larger transit providers also have to include the following items in their TAM plans:

- TAM and SGR policy

- Implementation strategy

- List of key annual activities

- Identification of resources

- Evaluation plan

What process must I follow to develop a TAM plan?

The TAM rule sets a process for developing a TAM plan that will vary depending on whether you are a Tier I or Two II provider, and whether you are preparing a TAM plan for only your own agency or your agency is participating in a group TAM plan. There are nine required elements to the TAM plan for a tier I provider. There are four required elements to the TAM plan for both groups and tier II providers. You will not submit your TAM plan to FTA, but you must share it with your planning organizations (e.g., Metropolitan Planning Organization, State Department of Transportation).

Does FTA require TAM plans to be submitted by October 1, 2018?

There is no formal submission requirement for the TAM plan on October 1, 2018, although it must be made available upon request. Following the October 1st deadline, transit providers are required to share their compliant TAM plans, along with SGR targets and asset condition information, with their State DOT and MPO planning partners. Since 2017 FTA has included TAM rule compliance in the annual Certifications and Assurances process, and grantees will be required to continue self-certifying compliance. In fiscal year 2019, the Triennial and State Management reviews will begin to include oversight of TAM rule compliance. For more information, please see the FAQ on TAM compliance.

All recipients and subrecipients of Federal Transit Administration (FTA) financial assistance that own, operate, or manage capital assets used for public transportation are required to have a TAM Plan in place by the deadline. Beginning October 1, 2018 FTA’s Certifications and Assurances will reflect all of 49 CFR 625 requirements, including a compliant TAM Plan. All FTA grantees are required to self-certify. Grantees that cannot self-certify due to a failure to comply with the TAM requirements may be unable to obligate a new grant in TrAMS.

What is the requirement for Board action for TAM plans?

The TAM rule only requires that an Accountable Executive approve the TAM plan. Any Board action is at the discretion of the grantee.

What level of change requires a complete TAM plan update?

If an agency experiences a significant unexpected change that cannot be addressed with a simple amendment to the existing TAM plan, a full TAM plan update (revision) is required. For example, asset damage from a hurricane, approval of a local tax for transit, or other changes to the TAM planning context would require a full update, whereas a new Accountable Executive might not. Agency TAM plans should establish thresholds for significant change based on their assets and policies, in order to ensure consistency in how updates occur and how often. These thresholds could be identified in Agreements with Stakeholders, the Evaluation Plan, and/or Group Plan Sponsor communication.

Does FTA require that TAM plans be signed by agency leadership?

There is no specific signature requirement for the TAM plan, although documented approval by the Accountable Executive is required. Agencies may determine the best way to present this documentation. For more information, please see the FAQ on TAM compliance.

Group TAM Plans

Who must be the sponsor of a group TAM plan?

Any direct recipient of Chapter 53 funds which passes along some or all of those funds to subrecipients that own or operate capital assets used in providing public transportation must sponsor a group TAM plan on behalf of any of its subrecipients that are not 5307 direct recipients themselves. Thus, in many instances, State Departments of Transportation and other designated recipients of Chapter 53 funds must be group TAM plan sponsors.

A direct recipient that is a tier I provider must also develop its own TAM plan independent of the group TAM plan it sponsors on behalf of tier II subrecipients. In rare instances, a tier II direct or designated recipient may have its own tier II subrecipients, in which case the direct recipient may both participate in and sponsor a single group TAM plan. See also Am I required to be a TAM group sponsor?

Who is allowed to participate in a group TAM plan?

All tier II subrecipients of Chapter 53 funds are eligible to participate in a group TAM plan. However, any tier II subrecipient that is also a direct recipient of Section 5307 Urbanized Area formula funds is not automatically included in any group TAM plan; it must request permission to participate in a group TAM plan. See Am I going to be a participant in a group TAM plan?

If a tribe only receives 5311(c) funds directly through FTA, then the State DOT is not required to solicit the tribe's participation in its group plan. However, if the tribe requests to participate, then the State DOT must accept the tribe into its group plan.

Where can I find more information about MPO Coordination and Statewide TAM Targets?

Please see the Metropolitan Planning Organization Responsibilities for the Transit Asset Management Rule FAQs.

TAM Asset Inventory

What assets must I include in a TAM asset inventory?

There are four categories of capital assets that must be included in a TAM asset inventory: facilities, equipment, rolling stock, and infrastructure. Your TAM plan must include an inventory of all the capital assets in each of the categories that you own, operate, or manage. More information on what assets must be included in your TAM asset inventory can be found in the “What do I need to report to the NTD” section of this FAQ.

In those instances where capital assets are shared among multiple transportation agencies, the agencies must determine, collectively, which of them is responsible for conducting the condition assessment of that asset, even though all of those agencies will be responsible for including that asset in their own asset inventories and in reporting data on that asset to the NTD.

Condition Assessments

What does “annual condition assessment report” in rule section 625.53(b) mean?

The annual condition assessment report refers to the annual data report to FTA's National Transit Database.

The TAM final rule requires you to assess all assets for which you have direct capital responsibility, including those that are owned by someone else but for which you have at least partial direct capital responsibility.

FTA requires that facility condition data be fully updated and reported to the NTD every four years, at a minimum. Agencies may choose to assess their facilities more frequently. However, at a minimum, they must report the condition of one quarter of the total number of their facilities to the NTD annually, and their condition assessments for the previous three years must include all of the facilities for which they have capital responsibility. Each annual report must include updated facility condition data incorporating any assessments completed since the last report.

Which facilities require a condition assessment?

The TAM final rule requires you to assess all facilities for which you have direct capital responsibility, including those that are owned by someone else but for which you have at least partial direct capital responsibility.

Administrative and maintenance facilities require a condition assessment only if the agency has capital responsibility for the facility and the transit use is greater than incidental. Use is incidental when 50 percent or less of the facility’s physical space is dedicated to the provision of public transportation service.

Exclusive-use maintenance facility means a maintenance facility that is not commercial and either owned by a transit provider or used for servicing their vehicles.

| Condition Assessment Required and Reported to NTD |

Condition Assessment Not Required |

|---|---|

|

|

What method must I use for conducting condition assessments of assets?

You can assess the condition of your assets in a way that is most useful to your agency. The TAM rule does not require a specific method for conducting condition assessments of assets.

It’s important to note that for facilities, you must report to the National Transit Database using the Transit Economic Requirements Model (TERM) condition assessment scale of 1-5. Under the TERM scale, an asset in need of immediate repair or replacement is scored as one (1), whereas a new asset with no visible defects is scored as five (5). Should you choose to use some other methodology for measuring the condition of your assets; you will need to convert the results of that assessment to the TERM scale for NTD reporting.

How do I know if I have direct capital responsibility for an asset?

You must consider the financial obligations you have to the condition of the asset. You must assess the condition of the assets listed in your asset inventory for which you have direct capital responsibility.

| You have direct capital responsibility | You do NOT have direct capital responsibility |

|---|---|

| You own the asset | You do not own the asset AND you are not responsible for replacing, overhauling, refurbishing, or conducting major repairs on that asset, or the costs of those activities are not itemized as a capital line item in your budget. |

| You jointly own the asset with another entity | |

| You are responsible for replacing, overhauling, refurbishing, or conducting major repairs on that asset, or the costs of those activities are itemized as a capital line item in your budget. |

NOTE: Performing minimal preventive maintenance work on an asset, like cleaning, does not in itself indicate that you have direct capital responsibility for the asset. An infrastructure asset itemized as capital line item in budget does not necessarily mean you have direct capital responsibility; you must also have management or oversight responsibilities for that line item project.

Do I have capital responsibility for a shared use facility?

We have two examples of shared use of facilities: 1) our contractor conducts maintenance for our revenue vehicles in a “shared” maintenance facility that we do not own; and 2) we share our administrative facility with other non-transit uses (e.g., we’re department of city government and our offices are in a small room in city hall). Do we have capital responsibility for the facility?

The fact that the asset is shared does not impact whether you have direct capital responsibility for the asset. If you own the facility, have a line item for the facility in your budget, or have recently paid for capital projects on the facility, then you have direct capital responsibility (see “How do I know if I have direct capital responsibility for an asset?”). If you do not have direct capital responsibility for the facility, then you must only include the facility in your TAM plan inventory (unless it is a passenger station or parking facility which are always included in the NTD inventory). If you use the facility but are not responsible for conducting or paying directly for major repairs, you do not have direct capital responsibility.

What must be reported when a facility is shared?

If you have any direct capital responsibility for the facility, then you must include the facility in your TAM plan inventory and your NTD asset inventory (A15 form). You must also report on the condition of the facility in your condition assessment, and include it in your performance targets and your investment prioritization. Further clarification of requirements for specific facility types are itemized below.

For Maintenance and Administrative facilities:

- Any maintenance or administration facility under 100 square-ft. does not need to be included (e.g. security guard shack, stand-alone restroom, storage shelter in which no work is performed) in either of your inventories.

- If your vehicles are the only vehicles that the maintenance facility services, then it is considered an “exclusive use” facility and thus must be inventoried in your TAM plan.

- If the administrative office is in a building that has only incidental transit use (e.g. city hall), then it is not required to be included in either of your inventories.

For Passenger and Parking facilities:

- All passenger facilities must be inventoried in your TAM plan and reported to the NTD regardless of ownership.

- You must inventory all parking facilities for which you have direct capital responsibility, and that are immediately adjacent to a passenger facility (e.g. a park-and-ride lot or a garage).

For a shared facility, you will coordinate with the other organizations with capital responsibility to determine a singular facility condition rating. Only one party needs to conduct the assessment; and all will report the assessed rating. For example, imagine you have a bus station based at a commuter rail facility and you provide funding to maintain the bus bays and passenger waiting area. If the rail operator conducts a condition assessment of the entire facility, rating it as a 4, both agencies would report a condition rating of 4 for the shared facility on their individual NTD (A-15) forms.

The performance measure for facilities is the percent of facilities rated below 3 on the TERM scale, it is not based on the size, value or your level of responsibility for the asset. Therefore, (continuing the previous example) the bus operator would include the bus station at the commuter rail facility as one asset the same as a facility that they wholly own, even though they only fund and use a portion of the facility. The A-15 form also includes a field to report the percent capital responsibility for the facility.

Your agency would set its target based on the all facilities included in the calculation of your performance measure, both shared and independently owned. The performance measures and targets do not need to match between the agencies that share capital responsibility for a facility.

Useful Life Benchmarks (ULBs)

What is a "useful life benchmark"?

Useful life benchmark (ULB) is the measure agencies will use to track the performance of revenue vehicles (rolling stock) and service vehicles (equipment) to set their performance measure targets. Each vehicle type’s ULB estimates how many years that vehicle can be in service and still be in a state of good repair. The ULB considers how long it is cost effective to operate an asset before ongoing maintenance costs outweigh replacement costs. ULBs are derived from FTA’s Transit Economic Requirements Model (TERM). The TERM model estimates the age at which each of the vehicle types would enter the SGR backlog, or have a rating of 2.5 or below on the TERM scale. See the table of useful life benchmarks here. These default ULBs will automatically populate in the NTD collection field. Alternatively, your agency can develop its own ULBs based on your operating conditions, warranty information, and any other criteria that would affect your assets’ maximum useful life.

What is the difference between TAM’s ULBs and the useful lifedefinition used in FTA’s grant programs?

The useful life under grant programs was set forth in the 2017 FTA Circular 5010.IE and refers to eligibility for replacement of an asset with FTA funds. For more information on useful life determination, review Award Management Requirements Circular 5010.1E and Program Circulars. The TAM ULB refers to the maximum age of the asset, or the point at which the asset enters the state of good repair backlog. The ULB is used solely for setting state of good repair performance measure targets for equipment and rolling stock asset categories.

The Default ULB Cheat Sheet states that transit agencies can adjust their ULB with approval from FTA. Can FTA provide guidance on the process?

When entering your fleet data in the NTD, you will have the option to either accept the pre-populated default ULBs or submit your customized ULBs. In cases where the ULB is significantly different from the default ULB value, you may be prompted to verify it is not a typo and/or submit justification for the value. If FTA accepts your NTD report, then it accepts your customized ULB.

Targets

What does a high or low performance target value mean?

For each of the four asset categories, FTA has defined performance measures to evaluate the performance of the assets within the category. You must set state of good repair (SGR) performance targets for certain assets within each category (see “What is the difference between assets in my TAM plan and NTD inventory and targets?” to determine which types of assets require performance targets).

For each asset category, the performance measure is a characterization of the percentage of the number of assets that are not in a state of good repair. For equipment and rolling stock, the performance measure is the percentage of vehicles that have met or exceeded their ULB. For infrastructure, the performance measure for rail fixed guideway, track, signals, and systems is the percentage of track segments with performance restrictions. For facilities, the performance measure is the percentage of facilities within an asset class, rated below condition 3 on the Transit Economic Requirements Model (TERM) scale.

All of the performance measures are designed with the goal of having low values. As the age increases or condition of assets deteriorates, the value of the performance measures will increase. To move toward a better state of good repair, you would want to set your targets to be lower than your current year’s performance measure value.

Lower Performance Measures Values = Better State of Good Repair

Who needs to approve the TAM Performance Measure targets before we submit them to the MPO?

The TAM Rule requires that the transit provider’s accountable executive approve its TAM plan, which includes the performance measure targets. Any other aspects of your approval process are considered a local decision.

Do MPOs have to update their TAM targets annually? Even if they update their TIP or MTP more frequently than Planning regulations require?

No, MPOs do not have to update their TAM targets annually. However, in consultation with the State DOTs and transit providers, they may choose to revise or maintain their performance targets when they update their TIPs or MTPs regardless of the frequency of those updates. Please note that FTA Planning regulations do not require MPOs to update their TIPs or MTPs annually.

MPOs are also not required to update or revisit their TAM targets every time a State DOT or transit provider updates its TAM targets. However, best practices would encourage consultation and communication with State DOTs and transit providers to ensure alignment of targets.

What is the difference between assets in my TAM plan and NTD inventory and targets?

Your TAM plan inventory will be more inclusive than the asset data you report to the NTD. The table below explains in detail which assets you need to include in which steps of your TAM plan and which to report to NTD.

| Assets |

TAM Plan Inventory |

NTD Inventory |

TAM Plan Condition Assessment |

SGR Targets |

|---|---|---|---|---|

| Revenue Vehicles | ||||

| Owned | yes | yes | yes | yes |

| Direct capital responsibility | yes | yes | yes | yes |

| 3rd party owned (direct capital responsibility) | yes | yes | yes | yes |

| 3rd party owned (NO direct capital responsibility) | yes | yes* | no | no |

| Equipment: Non-Revenue Vehicles (regardless of cost) | ||||

|

Owned |

yes | yes | yes | yes |

| Direct capital responsibility | yes | yes | yes | yes |

| 3rd party owned | no | no | no | no |

| Equipment: Over $50,000 Acquisition Value | ||||

| Owned | yes | no | yes | no |

| Direct capital responsibility | yes | no | yes | no |

| 3rd party owned | no | no | no | no |

| Equipment: Under $50,000 Acquisition Value | no | no | no | no |

| Facilities: | ||||

| Owned | yes | yes | yes | yes |

| Direct capital responsibility | yes | yes | yes | yes |

| 3rd party owned (direct capital responsibility) | yes | yes | yes | yes |

| 3rd party owned (NO direct capital responsibility) | yes | yes** | no | no |

| Infrastructure: Non Rail Fixed Guideway | ||||

| Owned | yes | no | yes | no |

| Direct capital responsibility | yes | no | yes | no |

| 3rd party owned (direct capital responsibility) | yes | no | yes | no |

| 3rd party owned (NO direct capital responsibility) | yes | no | no | no |

| Infrastructure: Rail Fixed Guideway | ||||

| Owned | yes | yes | yes | yes |

| Direct capital responsibility | yes | yes | yes | yes |

| 3rd party owned (direct capital responsibility) | yes | yes | yes | yes |

| 3rd party owned (NO direct capital responsibility) | yes | yes | no | no |

Other Assets

We have fixed guideway assets, but we don’t operate rail fixed guideway. Am I Tier I or Tier II? Do I need to set Infrastructure category targets?

If you do not operate rail fixed guideway public transportation, and if you do not have enough vehicles to qualify as a Tier I provider (see “Am I a Tier I or a Tier II Agency?” to determine your agency’s tier), then you would be considered a Tier II provider, even if you provide fixed guideway service like BRT or ferry service. As a Tier II provider, you are eligible to participate in a group TAM plan or develop an individual Tier II TAM plan (responsible for elements 1-4).

The infrastructure performance measure required by FTA is limited to railfixed guideway assets. Therefore, a transit provider that operates a fixed guideway service that is not rail-based (such as a BRT or ferry) would not have to set or submit a performance target for its non-rail infrastructure assets. Agencies may choose to set additional performance measures and targets for infrastructure as part of their TAM plans, although these are not required to be submitted to FTA.

The TAM infrastructure asset category includes infrastructure assets for all modes. The NTD has and will continue to collect data for all modes within the infrastructure category. However, BRT and ferry fixed guideway assets are not included in the expanded asset inventory for TAM performance measures. Please see the NTD Asset Inventory Module Reporting Manualfor more information regarding reporting requirements.

What does the $50,000 threshold refer to?

The $50,000 amount refers to the threshold for including non-vehicle equipment assets in the asset inventory. All non-revenue service vehicles are included as equipment assets, regardless of cost. You may exclude non-vehicle equipment assets with an acquisition value (original cost) under $50,000 from your asset inventory.

The $50,000 threshold does not apply to any other asset categories or to service vehicles. Therefore, you must include in your asset inventory all rolling stock, infrastructure, facilities (except bus stops), and service vehicles, regardless of their acquisition value.

Does the $50,000 threshold mean $50,000 in total equipment value, or $50,000 per unit of equipment?

If your program of capital projects or capital plan identifies equipment assets as individual units, or multiple line items, and each unit is less than $50,000, then you do not need to include each individual unit in your asset inventory. However, if your program of capital projects identifies equipment assets as one grouping of units or one line item and its value is greater than $50,000, then you must include it in your asset inventory.

For example, if your capital plan lists projects to purchase solar panels for 10 different park-and-ride lots and they are itemized as separate line items by location, each is likely to cost less than $50,000, and you are not required to include panels in the TAM inventory as an equipment asset. If, however, your capital plan lists the purchase of a new solar power system as one line item (purchasing 10 panels) that costs over $50,000, you would be required to list the system in your asset inventory.

What about equipment in a facility?

Equipment with an acquisition value between $10,000 and $50,000 may be considered part of an administrative or maintenance facility. If equipment is valued at $50,000 or more, or is a piece of equipment you would take to another location, it would be considered a separate equipment asset and not considered part of a facility.

Do information technology (IT) systems hardware and software need to be included in equipment category?

The final rule does not explicitly indicate how agencies should handle their IT hardware or software. If you want to create an asset class for systems and inventory your IT hardware and software, you are welcome to do so, but FTA does not endorse any specific approach to create an asset inventory of IT systems. However, the final TAM rule preamble suggests that systems belong in the infrastructure category. The FTA Transit Asset Management Guide includes systems under Infrastructure, and Chapter 5 of Appendix A, the Asset Management Guide Supplement, goes into greater detail regarding management of systems assets.